This morning, Arcep is delivering its annual “Telconomics” progress report on France’s telecoms market to coincide with the publication of the 2022 annual observatory. It includes key economic data on the French telecoms market, along with the fixed and mobile price index for 2022.

This event provides Arcep with an opportunity to:

- talk about the main workstreams that are underway, not least preparing for the next round of market analysis, covering 2024 to 2028, which will include monitoring and overseeing the legacy copper network switch-off;

- offer a reminder that the aim of Arcep regulation is to facilitate ongoing fixed and mobile superfast network rollouts in Metropolitan France and French overseas territories, thanks to efficient investments, notably through network sharing.

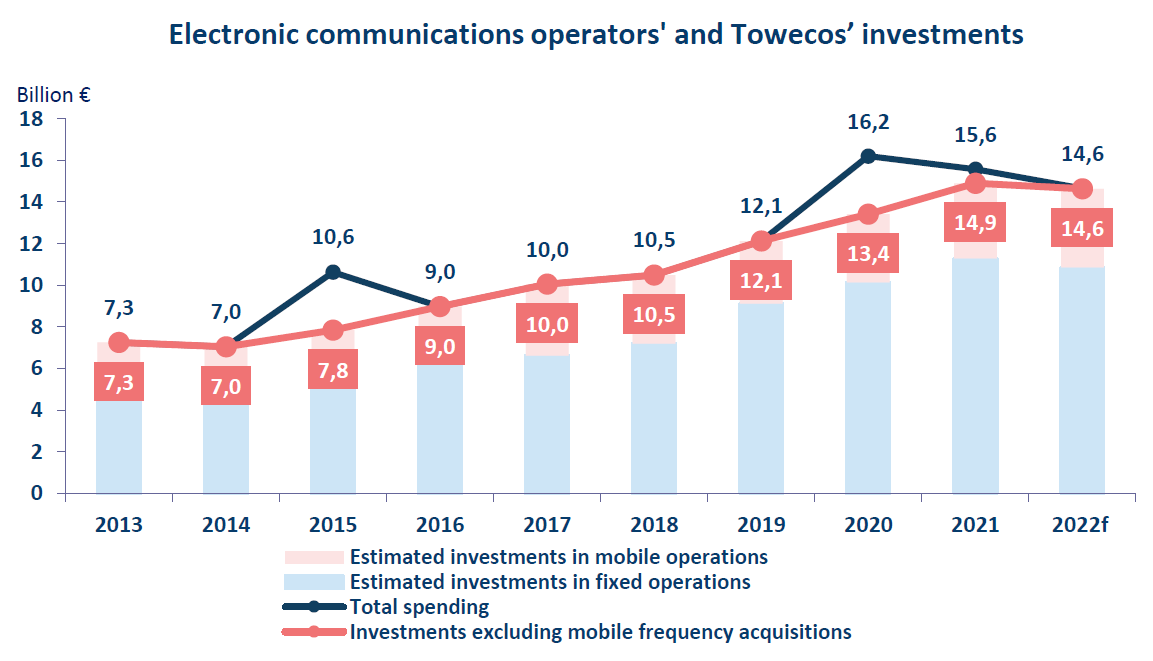

Spending by the sector’s stakeholders remained high in 2022

Electronic communications operators’ and mobile telephony infrastructure operators’ (towercos) investments in 2022 totalled 14.6 billion euros (excluding spending on 5G spectrum). This marks a decrease of 1.8% YoY while nevertheless remaining strong and above pre-2021 spending levels.

Among these investments, spending on superfast fixed and mobile local loop deployments stood at 8.1 billion euros, or 3.7% less than in 2021. This decrease can be attributed in particular to a slower rate of growth for the number of new premises being passed for fibre (+4.7 million in 2022 versus +5.4 million one year earlier).

High level of fixed and mobile network sharing

Seventy five percent of all premises passed for fibre have a choice between at least four operators, thanks to different co-investment schemes that both help foster investments and provide operators with guaranteed network access terms and conditions.

Forty seven percent of mobile network access infrastructure are shared in Metropolitan France, including 60% in rural areas. Arcep is in favour of an even greater degree of sharing in the most rural areas, particularly as it helps improve coverage and quality of service, and reduces the networks’ environmental footprint.

Operators’ revenue up by around 2%, for the second year in a row

Operators’ retail market revenue totalled 36.7 billion euros in 2022, increasing by around 2% for the second year in a row after 10 straight years of decline. The mobile market accounted for the totality of this increased revenue, thanks to both services and mobile device sales whose revenue climbed by around 5% YoY. Meanwhile, revenue from fixed services dropped slightly in 2022: by 0.3% YoY, after two years of weak growth. This trend is due to more sluggish growth for broadband and superfast broadband service sales (+2.4% in 2022, or -1-point YoY), which are not managing to fully offset declining narrowband service revenue (-15.4% in 2022).

Minor price hike for fixed and mobile access services in 2022

For the second consecutive year, residential mobile service prices increased only slightly in Metropolitan France: by 0.7% YoY. The rise in mobile service prices is due entirely to an increase in the price of unsubsidised plans (+1.6% YoY in 2022), which are hugely popular with operators’ customers (82%). The price of plans that include a subsidised handset has, however, decreased for the fourth year in a row – dropping by 3.4% in 2022.

As with mobile services, fixed line service prices increased only slightly in 2022, by 1.2% YoY, after having risen by a substantial 5.1% in 2021. DSL plans are one of the main sources of the price hike in 2022 (+ 3%), as certain offers have been eliminated in unbundled areas, thereby forcing customers to switch to more expensive plans. Meanwhile, the price of superfast access plans, most of which are fibre, increased by a mere 0.6% YoY.

FttH plans have outnumbered DSL plans since 30 June 2022, and 5G network use is growing

Of the total 31.9 million fixed network subscriptions, 18.1 million are based on fibre networks (+ 3.6 million YoY). Fibre thus represented 57% of all internet subscriptions in France at the end of 2022 (+ 11 points YoY). In addition, 8.2 million SIM cards were being used on 5G networks as of Q4 2022. They represent 10% of the 82.7 million mobile cards in service at the end of 2022 (+ 6 points YoY). The growth of 4G and 5G mobile network users goes hand in hand with a surge in data traffic on these networks. Of note, active customers on 4G networks generated an average 14 Gb of traffic a month in 2022, up 17% YoY.