This morning, Arcep is presenting its annual review of the status quo in France’s telecoms market, in addition to outlining the work being done at Arcep today, notably on network quality and availability across every region, on mobile network sharing, on “Achieving digital sustainability” and on Arcep’s increased involvement in the working being done at the European level (serving as BEREC Vice-Chair, work on the changes in the digital market and on environmental issues). This seventh edition of the “Telconomics” press conference coincides with the publication of the 2021 annual observatory, which includes key economic data on the French telecoms market, and of the fixed and mobile price index for 2021.

Spending by the sector’s stakeholders continues to climb

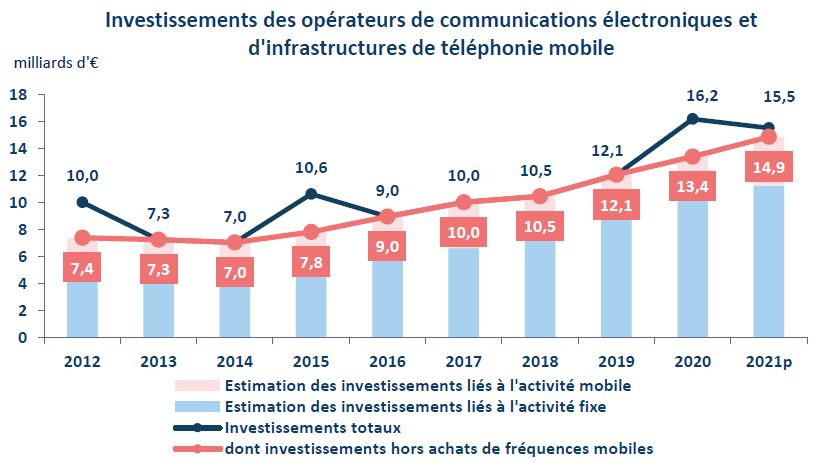

In 2021, operators’ investments (excluding spending on 5G spectrum) reached 14.9 billion euros, which marks a more than 10% increase YoY. Superfast fixed and mobile local loop deployments represent 8.5 billion euros in spending, or 12% more than in 2020.

After a 10-year decline, operators’ retail market revenue was back on an upwards trajectory in 2021 (+ 2.5%)

Retail market growth was driven chiefly by the mobile market. Mobile services revenue growth in 2021 stood at close to 5%, which can be attributed to a revival of roaming out starting in Q2 2021, and to handsets sales which returned to pre-Covid levels thanks to a 7% YoY increase in 2021. Operators’ increased revenue was also due to a lesser extent to the ongoing rise in fixed services revenue that began in 2020, and especially to the growth of broadband and superfast broadband plan sales: + 4% YoY in 2021.

Price hike for broadband and superfast broadband internet access services

Fixed service prices in the residential market in Metropolitan France increased for the second year in a row (+ 5% in 2021), while still remaining below price levels observed in 2018, after which they began to decrease sharply. The biggest price increases were on DSL-based plans (+7%), but the price of fibre plans also saw a 4% rise.

Mobile service prices remained largely unchanged, with a decrease in the price of plans that include a subsidised handset offsetting an increase in the price of unsubsidised plans.

Three million 5G network users; ongoing surge in mobile network data traffic

There were a total 80 million active SIM cards in use as of 31 December 2021. If the proportion of active SIM cards on 5G networks is still meagre (around 4% of the total, or around 3 million users), the number of 4G network users represent 82% of all active SIM cards – a number (66 million) that continues to increase steadily, at approximately 10% YoY.

Active customers on 4G networks continue to generate more and more mobile network traffic. In 2021, they consumed an average 12 Gb a month, which represents an increase of around 1 Gb per consumer compared to 2020. Data traffic generated by French mobile operators’ customers travelling abroad (i.e. roaming out) skyrocketed in 2021 (+ 50% YoY) after having plummeted in 2020 (- 17%) due to travel restrictions during the pandemic, and is now significantly higher than before the Covid-19 crisis.

Optical fibre: fibre-based internet plans outnumbered DSL plans for the first time in 2021

In the fixed services market, internet subscription growth in 2021 is due entirely to the increase in fibre subscribers. There were a total 14.5 million active fibre access lines at the end of 2021, which represents a YoY increase of 4.1 million. This means that, for the first time, there were more active fibre-based broadband and superfast broadband lines in France than copper network DSL-based ones (which totalled 14.4 million).

As of 31 December 2021, of the total 31.5 million fixed internet access lines, 18.4 million are superfast access lines (58%, + 10 points YoY), the vast majority of which are FttH (79%).